How to Structure a Husband-Wife LLC as a Disregarded Entity: A Step-by-Step Guide

Structure a Husband-Wife LLC as Disregarded Entity: Step-by-Step Guide - Qualify, Plan & Understand Legal/Tax Implications for Simplified Tax Filing.

March 31, 2025

Starting a business with your spouse can be both rewarding and practical. When you set up an LLC together, you have several options for how the IRS will treat your business for tax purposes.

An LLC co-owned by spouses can be treated as a disregarded entity rather than a partnership. This significantly simplifies tax filing and potentially saves you money each year.

Understanding the requirements for qualifying as a disregarded entity is crucial before proceeding. The rules differ depending on whether you live in a community property state like Texas or in a non-community property state such as Iowa.

Setting up your husband-wife LLC properly requires careful planning and consideration of both legal and tax implications.

The process involves more than just paperwork—it requires understanding how ownership percentages, operating agreements, and state laws affect your business structure.

Key Takeaways

Need help with this topic?

Why Choose A Husband-Wife LLC?

A husband-wife LLC provides couples with flexibility in structuring their business for tax purposes. In community property states, spouses can elect to have their LLC treated as a "disregarded entity" for federal tax purposes despite having two owners.

This simplified tax treatment means couples can avoid filing partnership tax returns while maintaining joint ownership benefits. They can report business income directly on their personal tax returns using Schedule C.

Couples also benefit from shared decision-making authority and the ability to divide responsibilities based on each person's strengths. This arrangement creates clear ownership rights for both spouses.

For retirement planning, a husband-wife LLC can establish retirement accounts that benefit both parties while potentially maximizing tax advantages.

Liability Protection And Asset Separation

The primary advantage of forming an LLC is its liability protection to both spouses. This protection creates a legal barrier between personal and business assets.

If the business faces lawsuits or debt collection, creditors generally cannot access:

- Personal bank accounts

- Family homes

- Personal vehicles

- Retirement accounts

- Other personal possessions

This protection works both ways. Business assets typically remain protected from personal creditors if spouses face financial difficulties.

This arrangement offers married entrepreneurs peace of mind and ensures that family assets remain secure while building a business together.

The LLC structure separates business and personal finances, which is crucial for maintaining liability protection.

Proper documentation and adherence to LLC formalities are essential to ensure this protection remains intact.

What Is A Disregarded Entity?

A disregarded entity is a specific tax classification that can significantly simplify how your business reports income and pays taxes.

This status is particularly beneficial for husband-wife-owned LLCs that meet certain requirements.

Definition And Tax Implications

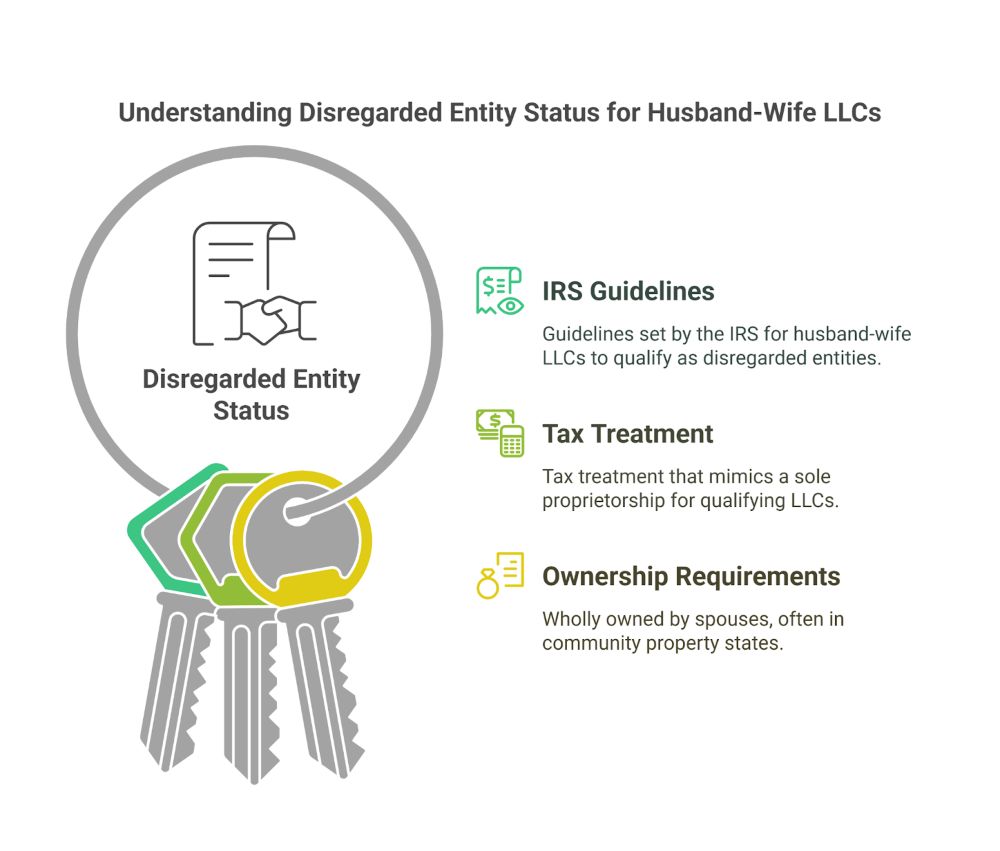

A disregarded entity refers to a business that the IRS treats as if it doesn't exist for tax purposes. For an LLC, this means the IRS "disregards" the separate legal entity and treats it as an extension of its owner.

For a single-member LLC or a qualified husband-wife LLC, this tax treatment mimics that of a sole proprietorship.

The IRS has specific guidelines for husband-wife LLCs seeking disregarded entity status:

- The LLC must be wholly owned by the spouses

- In community property states, the business must qualify as community property

- Both spouses must report all income, gains, losses, and deductions on their joint tax return

This classification protects your assets while avoiding the complexity of partnership taxation.

How Disregarded Entity Status Simplifies Tax Reporting

Choosing disregarded entity status offers significant advantages for tax reporting.

Instead of filing a separate business tax return, all business income and expenses are reported on Schedule C, which is attached to the couple's personal Form 1040.

Key benefits include:

- No need to file Form 1065 (Partnership Return)

- Avoids complex partnership tax rules

- Simplifies bookkeeping requirements

- Eliminates separate employer identification number (EIN) requirements in many cases

This classification is particularly advantageous for spouses in community property states, as it allows them to maintain equal ownership without partnership complications.

Business owners save time and potentially reduce tax preparation costs while maintaining the liability protection benefits of an LLC structure.

Overview Of LLCs For Married Couples

Married couples have unique options for structuring a Limited Liability Company (LLC), which can provide tax advantages and simplified filing requirements.

These options depend on state laws, particularly whether you live in a community property state.

What Makes An LLC Attractive For Husband-Wife Teams

LLCs offer married couples significant flexibility in how their business is taxed. In many cases, a husband-wife LLC can be treated as a disregarded entity rather than a partnership. This simplifies tax filing requirements.

For couples in community property states, an LLC can be treated as a single-member LLC (SMLLC) for federal tax purposes. This means the business doesn't file a separate tax return.

Instead, all business income and expenses flow directly to the couple's tax return (Form 1040) via Schedule C. This arrangement eliminates the need to file partnership returns.

Couples may also form a Qualified Joint Venture, allowing them to avoid partnership tax treatment while recognizing both spouses as business participants. This option is available if:

- Both spouses are the only owners

- Both materially participate in the business

- Both elect not to be treated as a partnership

Legal And Financial Benefits Specific To Married Business Owners

A properly structured husband-wife LLC provides excellent liability protection while maintaining tax efficiency.

The LLC shields personal assets from business debts and liabilities, protecting the couple's home, savings, and other personal property.

When structured as a Qualified Joint Venture LLC, both spouses receive Social Security and Medicare credit for their work. This ensures both partners build retirement benefits through their business activities.

Filing as a disregarded entity or joint venture also saves money on preparation costs since complex partnership returns are not needed. This can significantly reduce accounting expenses.

The IRS provides additional flexibility for couples in community property states. If the business meets the criteria of a "qualified entity," spouses can choose whether to treat it as a disregarded entity or a partnership.

In non-community property states, husband-wife LLCs are typically treated as multi-member LLCs by default, but the Qualified Joint Venture election can override this treatment..

Key Benefits Of Disregarded Entity Status

Structuring a husband-wife LLC as a disregarded entity offers significant advantages for married couples in business together.

This status provides streamlined tax reporting, administrative simplicity, and strong asset protection while maintaining the LLC's liability shield.

Simplified Tax Filing (Reporting On Schedule C For Qualified Joint Ventures)

A husband-wife LLC, which is treated as a disregarded entity, allows for much simpler tax reporting.

Instead of filing a separate partnership tax return (Form 1065), the business income and expenses are reported directly on the couple's tax return.

For qualified joint ventures, spouses can each file their own Schedule C for their respective shares of the business. This approach eliminates the need to prepare and file partnership returns, saving both time and potential accounting costs.

Each spouse reports their share of profits and losses on their individual Schedule C, allowing them to receive proper Social Security and Medicare tax credits.

This arrangement benefits couples in community property states, where the IRS automatically treats a jointly owned LLC as a disregarded entity.

Reduced Administrative Burdens And Compliance Benefits

Disregarded entity status substantially decreases administrative paperwork and compliance requirements. The simplified tax filing process eliminates the need to:

- File separate business tax returns

- Issue K-1 forms

- Maintain complex partnership accounting records

- File quarterly partnership estimates

Couples can avoid partnership tax rules, which often require specialized accounting knowledge. This translates to lower accounting and tax preparation fees and reduced time spent on administrative tasks.

Business owners can focus more on growing their business than managing complex tax compliance issues.

For many husband-wife businesses, this administrative simplicity represents one of the most compelling reasons for electing disregarded entity status.

Protection Of Personal Assets Without Complex Tax Filings

A husband-wife LLC classified as a disregarded entity protects personal assets while maintaining tax simplicity. This creates an ideal balance between liability protection and ease of operation.

The LLC structure creates a legal separation between business and personal assets, protecting the couple's property from business creditors and lawsuits. This liability shield remains intact despite the simplified tax treatment.

Unlike sole proprietorships or general partnerships, which offer no liability protection, the LLC structure ensures business obligations cannot typically be enforced against the owners' personal assets.

This protection exists regardless of whether the LLC is treated as a partnership or disregarded entity for tax purposes.

The disregarded entity status combines the best of both worlds: the liability protection of a formal business entity with the tax simplicity of a sole proprietorship or qualified joint venture.

Determining Eligibility For Disregarded Entity Status

For husband-wife LLCs, meeting specific IRS requirements is essential to qualify as a disregarded entity.

This status offers significant tax simplification but depends on several key factors, including ownership structure and state property laws.

Criteria Under IRS Rules For A Husband-Wife LLC

To qualify as a disregarded entity, a husband-wife LLC must be wholly owned by the spouses as community property under state, foreign country, or U.S. possession laws. This requirement is fundamental and non-negotiable.

The business must operate in a community property state (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, or Wisconsin). In these states, property acquired during marriage is typically considered jointly owned.

For example, a husband-wife LLC based in Texas may qualify for disregarded entity status automatically. In contrast, Iowa couples would need to explore alternate structures like a Qualified Joint Venture or partnership.

Both spouses must:

- Have 100% ownership of the LLC between them

- Have not elected to treat the entity as a corporation

- File taxes appropriately based on their disregarded entity status

If these criteria aren't met, the IRS may classify the LLC as a partnership by default, requiring different tax filings.

Impact Of Filing Status (Married Filing Jointly Vs. Separately)

The tax filing status of the spouses significantly affects the treatment of the disregarded entity.

Married filing jointly is typically the preferred option for couples with a disregarded entity LLC, as it aligns with the concept of treating business income as belonging to a single taxpayer unit.

When filing jointly, business income and expenses flow directly to the joint tax return, simplifying tax preparation. The income is reported on Schedule C, E, or F (depending on the business type) of Form 1040.

On the other hand, if spouses choose to file separately, the IRS may question whether the entity truly qualifies as disregarded, potentially forcing a partnership classification.

Tax professionals often recommend consulting an expert before choosing to file "married filing separately" with a husband-wife LLC to avoid unintended tax consequences.

Step-By-Step Guide To Structuring Your Husband-Wife LLC

Step 1: Choose A Business Name And Verify Availability

Selecting the right name for your husband-wife LLC is crucial as it establishes your brand identity and must comply with state regulations.

Before filing any paperwork, you must verify that your chosen name is available and meets all legal requirements.

Tips For Selecting A Unique, Compliant Business Name

When choosing a name for a husband-wife LLC intended to be a disregarded entity, couples should consider both branding and legal compliance.

The name must include a business entity suffix such as "LLC," "Limited Liability Company," or state-specific variations.

Effective LLC names typically:

- Reflect the business purpose or values

- Are easy to spell, pronounce, and remember

- Avoid potentially confusing similarities with existing businesses

- Don't contain restricted words that require additional licenses

When naming their LLC, spouses should consider future expansion possibilities. A too-specific name might limit growth opportunities. If an online presence is planned, it's also wise to check domain name availability.

How To Check State-Specific Business Name Databases

Most states maintain searchable databases of registered business entities through their Secretary of State websites.

Checking LLC name availability involves searching these databases to ensure no other business uses your desired name.

Step 2: File The Articles Of Organization

Filing your Articles of Organization is a critical step that officially establishes your husband-wife LLC.

This document registers your business with the state and begins your legal existence as a limited liability company.

Filing Requirements With Your State's Secretary Of State

Every state requires LLCs to file Articles of Organization (sometimes called Certificate of Organization) with the Secretary of State's office.

The filing process typically involves submitting the required forms either online, by mail, or in person.

Filing fees vary by state, typically from $50 to $500. Processing times also differ significantly—some states offer same-day processing, while others may take several weeks. Many states now provide expedited processing for an additional fee.

Most states maintain dedicated business formation websites where couples can complete the entire filing process electronically. These portals often include form templates and step-by-step instructions to simplify the process for new business owners.

It's advisable to check the specific requirements in your state before beginning the filing process.

Key Information Required In The Articles Of Organization

The Articles of Organization typically require several essential pieces of information about your husband-wife LLC:

- LLC name and address: The official name must include "LLC" or "Limited Liability Company" and a physical business address.

- Names and addresses of members: Both spouses' information as the LLC owners.

- Registered agent information: Name and address of the person authorized to receive legal documents.

- Business purpose: A statement describing the LLC's activities.

- Management structure: Specify if the LLC is member-managed (by the spouses) or manager-managed.

For husband-wife LLCs seeking disregarded entity status, it's important to document clearly that both spouses have ownership interests. Some states may require you to specify the ownership percentages.

The Articles should also include the duration of the LLC (typically "perpetual") and the date when business operations will commence.

Step 3: Draft A Comprehensive Operating Agreement

An operating agreement serves as the foundation for your LLC's operations and governance. This essential document outlines how you and your spouse manage the business and make important decisions.

An operating agreement is crucial even when not legally required by your state. This document clearly establishes ownership percentages between spouses, preventing future disagreements about business contributions.

Management structures should be explicitly defined. Couples can choose either member-managed (both actively involved) or manager-managed (one spouse handles daily operations) arrangements based on their skills and availability.

Dispute resolution procedures are vital for marital business partnerships. Include clear processes for resolving disagreements through mediation before costly litigation.

The operating agreement should also address what happens to the business during major life changes like divorce or death. Thoughtful planning now can prevent painful complications later.

Special Clauses For Husband-Wife Dynamics And Tax Treatment

Husband-wife LLCs benefit from specialized clauses addressing their unique relationship. Consider including provisions for vacation policies, work-life balance, and role flexibility that accommodate family responsibilities.

Tax treatment confirmation is essential. The agreement should explicitly state the intent to be treated as a disregarded entity for federal tax purposes, documenting your planned taxation method.

Include detailed profit distribution methods. While 50/50 splits are common, some couples prefer distributions based on work contributions or specialized skills.

Decision-making thresholds deserve careful consideration. Determine which decisions require mutual consent and which can be made independently by either spouse.

Regular review clauses ensure the agreement evolves with your business and relationship. Schedule annual reviews to keep the document current as your circumstances change.

Step 4: Apply For An EIN (Employer Identification Number)

Obtaining an Employer Identification Number is essential for most LLCs, even those structured as disregarded entities.

This unique nine-digit number helps identify your business for tax purposes and is required for specific banking and filing activities.

When An EIN Is Necessary, Even For Disregarded Entities

Though your husband-wife LLC is a disregarded entity for federal tax purposes, you'll still need an Employer Identification Number (EIN) in several common situations:

- Opening a business bank account (most financial institutions require it)

- Hiring employees (even if planning to do so in the future)

- Filing certain tax returns like excise tax forms

- Changing your LLC's classification later on

- State-level requirements regardless of federal status

Many spouse-owned LLCs initially think they can operate using just a Social Security Number, but this limits growth opportunities and professional credibility.

Step 5: Elect The Appropriate Tax Treatment

Selecting the right tax treatment for your husband-wife LLC is crucial for maximizing tax benefits and simplifying your filing requirements.

The IRS offers specific options for married couples that can significantly reduce paperwork and potentially lower your tax burden.

How To File As A Disregarded Entity (Or A Qualified Joint Venture In Community Property States)

In community property states, husband-wife LLCs can be treated as disregarded entities for federal tax purposes.

To qualify, spouses must wholly own the business as community property. In this case, no separate tax election form is needed.

To file as a disregarded entity:

- Form 1040 - Report all business income and expenses on Schedule C

- Single EIN - Use one Employer Identification Number for the business

- Self-Employment Tax - Each spouse reports their share of self-employment income

For qualified joint ventures, spouses should divide income, gains, losses, deductions, and credits according to their respective interests in the venture. Each spouse must file a separate Schedule C, but no partnership return is required.

Options If Your State Does Not Recognize Disregarded Status For Married Couples

If your state doesn't recognize disregarded status for married couples, several options remain available. Couples in non-community property states like Iowa must take extra care to structure their LLCs properly.

By default, a husband-wife LLC in Iowa would be treated as a multi-member LLC—requiring a partnership return (Form 1065)—unless the couple elects Qualified Joint Venture status.

This election allows each spouse to file a separate Schedule C while avoiding the complexity of partnership tax filings.

Option 1: File as a Partnership

- File Form 1065 (Partnership Return) for federal taxes

- Issue Schedule K-1s to both spouses

- Follow state requirements for partnership filing

Option 2: Qualified Joint Venture Election

- Available in non-community property states if you elect out of partnership treatment

- Both spouses must own at least 50% of the business as qualified joint venture members

- File separate Schedule Cs based on ownership percentage

Option 3: Single Member Structure

- Consider placing 100% ownership with one spouse

- Other spouse can be an employee or an independent contractor

- Simplifies filing but may affect liability protection

Consult a tax professional to determine which approach best fits your situation and state requirements.

Step 6: Maintain Ongoing Compliance

After establishing your husband-wife LLC as a disregarded entity, ongoing maintenance is essential to preserve its legal status and tax benefits.

Proper compliance ensures your business continues to operate smoothly and maintains the liability protection you've established.

Annual Filings, State Fees, And Record-Keeping Requirements

Most states require LLCs to file annual or biennial reports with the Secretary of State's office. These filings typically include basic company information and require payment of state fees that vary by location.

Filing deadlines are strict, and missing them can result in penalties or even administrative dissolution.

As a disregarded entity, couples must maintain clear financial records that separate business and personal finances. This includes:

- Dedicated business bank accounts

- Proper bookkeeping systems

- Documentation of business expenses

- Records of capital contributions

Tax requirements remain streamlined compared to partnerships, but spouses should still track business income on Schedule C with their tax returns. The IRS allows reporting on either spouse's return in community property states.

Best Practices For Keeping The LLC's Structure Intact Over Time

Maintaining proper documentation is crucial for preserving disregarded entity status. Couples should create and follow an Operating Agreement clearly stating their ownership structure and business relationship.

Regular business meetings with written minutes help demonstrate that the LLC is being operated properly. These records become especially important if the IRS ever questions your entity classification.

Avoid commingling personal and business funds at all costs. This is one of the fastest ways to lose liability protection through what courts call "piercing the corporate veil."

When acquiring new properties or business assets, ensure they're properly titled to the LLC. This strengthens asset protection and maintains clear ownership boundaries.

Consider scheduling annual compliance reviews with an attorney or tax professional. These experts can identify potential issues before they become problems and help ensure your husband-wife LLC maintains its disregarded entity status.

How Income Is Reported For A Disregarded Entity

When a husband-wife LLC is classified as a disregarded entity, the IRS doesn't recognize it as separate from its owners for tax purposes.

The tax reporting process becomes streamlined, with business income flowing directly to the owners' tax returns.

For a disregarded entity LLC, business income and expenses are reported directly on the owners' personal tax return (Form 1040). Since the LLC is "disregarded," it doesn't file its own tax return.

For husband-wife LLCs in community property states that qualify as disregarded entities, the couple reports business activities on their joint tax return. This is possible when the LLC is wholly owned by a husband and wife as community property and they file jointly.

The type of business determines where the income appears on the tax return. For most businesses, owners report income and expenses on Schedule C (Profit or Loss From Business). Rental properties use Schedule E instead.

Specific Forms And Schedules Required By The IRS

The primary form for reporting disregarded entity income is Form 1040 (U.S. Individual Income Tax Return), but several schedules may apply:

- Schedule C: Used for reporting business profit or loss

- Schedule E: For rental real estate, royalties, and pass-through entities

- Schedule SE: Required for calculating self-employment tax when owners materially participate in the business

Self-employment tax applies to disregarded entity income unless the business activity is exempt. The owners must pay both the employer and employee portions of Social Security and Medicare taxes.

Although the LLC is disregarded for income tax purposes, it remains separate for employment taxes if it has employees. In such cases, the LLC must obtain its own EIN and handle payroll tax filings.

Potential Pitfalls And How To Avoid Them

Setting up a husband-wife LLC as a disregarded entity offers tax advantages, but several potential complications can arise if it is not structured correctly and maintained. Understanding these challenges beforehand can help spouses avoid costly mistakes with the IRS.

Common Errors In Classification And Reporting

Many couples mistakenly assume their LLC automatically qualifies as a disregarded entity simply because they're married. However, the IRS has specific requirements that must be met. Under applicable state laws, the business must be wholly owned as community property.

Non-community property states present additional challenges. In these states, spouses often incorrectly file as a disregarded entity when they should file as a partnership, potentially triggering IRS scrutiny.

Another common error is inconsistent reporting. Some couples file individual Schedule C forms when they should submit Form 1065 for partnerships. This inconsistency may raise red flags during an audit.

Key prevention strategies:

- Verify your state's community property status before classification

- Document ownership percentages clearly in operating agreements

- Maintain separate business accounts and records

- File consistent tax forms year-to-year

When To Consult A Tax Professional For Optimization

Tax professionals should be consulted when establishing a husband-wife LLC to determine if it meets the "qualified entity" criteria.

These professionals can identify if your arrangement satisfies Revenue Procedure 2002-69 requirements.

Professional advice becomes particularly crucial when:

- One spouse wants to contribute to the business as an employee rather than owner

- The couple lives in a non-community property state

- Business income exceeds $150,000 annually

- The couple owns multiple businesses together

A tax professional can help determine whether electing partnership status might actually provide better tax benefits than disregarded entity status in certain situations. They can also identify potential liability issues that might arise from treating the LLC as a single entity.

Annual tax planning meetings ensure compliance with changing regulations and maximize available deductions for spousal business owners.

When To Consult A Business Attorney

While a husband-wife LLC can offer simplicity as a disregarded entity, certain situations require professional guidance to ensure compliance and maximize benefits.

Identifying Red Flags That Signal The Need For Professional Guidance

Complex Business Changes

- Business expansion beyond state lines

- Adding employees or contractors

- Significant changes in revenue or assets

- Changes in ownership structure

Tax Complications

- Uncertainty about filing as a disregarded entity vs. a partnership

- Questions about Schedule C vs. Schedule E reporting

- Residence in a non-community property state

Couples should seek professional help when moving between states, especially when relocating from a community property state to a non-community property state. This change can affect the LLC's tax treatment and may require restructuring.

Benefits Of Regular Legal And Tax Check-Ups

Preventative Protection

Regular consultations with professionals can identify potential issues before they become problems. Annual reviews ensure continued qualification as a disregarded entity and compliance with changing laws.

Optimization Opportunities

Professionals can identify tax-saving strategies specific to husband-wife LLCs. A CPA can help maximize deductions while maintaining proper documentation to support the LLC's disregarded status.

Peace of Mind

Working with experts provides confidence that the business structure remains optimized for both tax efficiency and asset protection. This allows couples to focus on growing their business rather than worrying about compliance issues.

Establishing relationships with a business attorney and CPA creates a support team that understands the specific needs of a husband-wife LLC and ensures continuity of advice as the business evolves.

Wondering how to structure your husband-wife LLC to gain the tax benefits of a disregarded entity? Don’t worry—I’ve got you covered. Use this step-by-step checklist to ensure you’re on track with every legal requirement and documentation needed.

| Action Step | Details | Completion |

| Determine if your state is a community property state (e.g., Arizona, California, Texas). | Check state laws to confirm eligibility for disregarded entity status. | __________ |

| Decide on the business structure that best fits your goals (e.g., LLC vs. Qualified Joint Venture). | Consider liability, tax benefits, and long-term goals. | __________ |

| Evaluate the tax and legal benefits of a disregarded entity status. | Consult with a tax professional for specific financial impacts. | __________ |

| Consult with a business attorney or tax professional to confirm eligibility and benefits. | Schedule an initial consultation for tailored advice. | __________ |

| Choose a unique and compliant business name for your LLC. | Ensure the name aligns with branding and state regulations. | __________ |

| Verify the business name availability with your state's Secretary of State. | Use the online database or contact the office directly. | __________ |

| Draft and file the Articles of Organization with all required state-specific information. | Include member names, business purpose, and management structure. | __________ |

| Create a comprehensive operating agreement that includes ownership percentages, management roles, and dispute resolution protocols. | Document profit-sharing, tax elections, and exit strategies. | __________ |

| Obtain an EIN from the IRS if needed for business banking, hiring employees, or tax purposes. | Apply online at the IRS website for quick processing. | __________ |

| Determine if you qualify for disregarded entity status and file taxes on Schedule C. | Complete IRS requirements and maintain proper records. | __________ |

| Explore partnership or Qualified Joint Venture options if not in a community property state. | Evaluate tax implications and compliance requirements. | __________ |

| File annual or biennial reports with the Secretary of State. | Mark your calendar to avoid late fees and penalties. | __________ |

| Maintain proper financial records and avoid commingling personal and business funds. | Use separate bank accounts and accounting systems. | __________ |

| Conduct regular business meetings and keep minutes for compliance. | Store meeting records safely for potential audits. | __________ |

| Schedule annual reviews with a tax professional to ensure ongoing compliance. | Update records and adjust strategies as needed. | __________ |

| Regularly review and update your operating agreement. | Reflect changes in ownership, roles, and responsibilities. | __________ |

| Monitor changes in state laws that might affect your LLC’s status. | Stay informed through legal updates or a business attorney. | __________ |

| Avoid inconsistent tax filings to maintain disregarded entity status. | Double-check filings for accuracy and compliance. | __________ |

| Consult a legal or tax professional when considering major business changes. | Protect your LLC status and avoid unintended consequences. | __________ |

Conclusion

Setting up a husband-wife LLC as a disregarded entity can offer significant tax advantages while maintaining solid liability protection.

When structured correctly in a community property state, couples can avoid the complexity of partnership tax filings.

Remember that the business must qualify as a "qualified entity" according to IRS guidelines. This means the LLC must be wholly owned by the spouses as community property under state law.

Couples should consult with a tax professional before making any final decisions. Each family's situation is unique, and what works for one couple may not be optimal for another.

Regular compliance with state regulations remains essential even with disregarded entity status.

Annual reports, maintaining separation of personal and business finances, and other LLC formalities must still be observed.

The streamlined tax processes make this structure attractive for many married business owners.

Filing taxes as a disregarded entity simplifies reporting on Schedule C, which is included with the couple's personal tax return.

This structure provides a solid foundation for spouses planning to grow their business together.

It combines the simplicity of sole proprietorship taxation with the robust liability protection of an LLC.

Frequently Asked Questions

What Is a Disregarded Entity for a Husband-Wife LLC?

A disregarded entity allows a husband-wife LLC to be treated as a sole proprietorship for tax purposes. This enables simplified tax filing by enabling the owners to report business income directly on their personal tax returns.

What Are the Benefits of Structuring a Husband-Wife LLC as a Disregarded Entity?

Key benefits include simplified tax reporting, avoidance of partnership tax returns, reduced administrative burdens, and robust liability protection for personal assets.

How Can a Husband-Wife LLC Qualify as a Disregarded Entity?

The LLC must be wholly owned by the spouses as community property; they must file jointly, and the business should meet IRS guidelines for a "qualified entity" in a community property state.

What Are Community Property States, and Why Do They Matter for a Disregarded Entity?

Community property states—such as Texas, California, and Arizona—automatically treat a husband-wife LLC as a disregarded entity, simplifying tax reporting.

In contrast, non-community property states like Iowa typically treat a jointly owned LLC as a partnership unless specific steps are taken to elect otherwise.

Do Husband-Wife LLCs Need an EIN if Treated as a Disregarded Entity?

No separate EIN is generally required unless the LLC has employees or needs it for banking purposes. Otherwise, the business can often use the owners’ Social Security numbers for tax filings.

What Documentation Is Needed to Maintain a Disregarded Entity Status?

To maintain this status, a clear operating agreement, adherence to state LLC requirements, and proper record-keeping of business transactions separate from personal finances are essential.

When Should a Husband-Wife LLC Consider Consulting a Business Attorney?

Legal guidance is recommended when forming the LLC, drafting operating agreements, navigating state-specific regulations, and during major business transitions like expansion or restructuring.