Don’t Launch Without This: Your Guide to Founder Agreements and Bylaws

If you want your startup to run smoothly and avoid future disputes, founder agreements and bylaws are must-have documents right from the start.

These tools help you and your co-founders set clear expectations about roles, responsibilities, and ownership.

Taking the time to define these early can save you from misunderstandings and legal problems as your business grows.

Founder agreements ensure that everyone is clear about their expectations and help prevent personal conflicts. Bylaws provide the foundation for how your company makes decisions and handles challenges.

To give your business the best chance to succeed, it’s smart to put these basic rules in place as soon as you form your company.

Many founders don’t realize the value of these documents until it’s too late.

Avoid common mistakes and establish the groundwork now, so your focus can stay on building your business, rather than fixing problems that could have been prevented.

Key Takeaways

- Founder agreements and bylaws prevent disputes, lawsuits, and startup failure.

- They’re required or expected by banks, investors, and even tax authorities.

- Templates don’t cut it, Texas startups need genuine, legally binding documents that hold up.

- Surge Business Law offers startup-focused flat-fee packages to handle this from day one.

What Is a Founder Agreement and Why Does It Matter?

A founder agreement sets the basic rules for how you and your co-founders will work together, split responsibilities, and protect each other from future conflict.

By making things clear early on, you avoid misunderstandings and legal issues that can harm your business later.

Defining the Relationship Between Co-Founders

A founder agreement is a legal agreement between business partners. It outlines the responsibilities of each co-founder and the rights and privileges each person has within the startup.

This contract sets the foundation for your business relationship. The agreement addresses key questions, such as who owns what percentage of the company, how decisions are made, and what happens if someone wants to leave.

This helps everyone stay on the same page. This document also outlines how founders will collaborate, resolve disputes, and define each person’s daily responsibilities.

Having a clear legal framework in place from the start protects your business if issues arise between you and your partners.

Key Clauses Every Founder Agreement Should Contain

Some clauses should be included in every founder or co-founder agreement. These protect you and set up your company for success.

The most important clauses include:

- Equity Split: Defines how much of the company each founder owns and how those shares can change if someone leaves early.

- Vesting Schedule: Outlines the rules for earning equity over time, similar to a startup founder vesting agreement, which can help keep founders motivated to stay.

- Roles and Responsibilities: Lists who is in charge of which parts of the business, such as finance, product, or marketing.

- Decision Making: Explains how major business choices are made or how to break a tie.

- IP Ownership: Specifies who owns the company’s ideas, inventions, and trademarks (founder IP ownership).

- Exit Terms: Details what happens if a founder quits, is fired, or sells their shares.

Including these clauses helps protect founders and the business from conflict and confusion.

How Founder Agreements Differ From Operating Agreements or Shareholder Agreements

Founder agreements differ from operating agreements and shareholder agreements. A founder agreement comes first, before the company is fully formed.

It is focused on the goals, contributions, and rights of the founders. An operating agreement is mostly for LLCs. It outlines the rules for operating the entire company after it’s officially established.

A shareholder agreement is for corporations. It manages the rights and responsibilities of individuals who own shares in the company, which can include investors, employees, or both, not just the founders.

Founder agreements often address unique early-stage issues, such as setting up the initial equity split, founder IP ownership, and key responsibilities.

As your business grows, you may need to establish new documents, such as bylaws or an operating agreement, to align with your company’s structure.

Start with Surge Business Law today and get your custom founder agreement and bylaws—no hourly rates, just transparent flat fees. Contact us now.

What Are Corporate Bylaws and When Are They Required?

Corporate bylaws establish the rules for running your business daily and help you avoid confusion or conflict in the future.

In most states, including Texas, corporations are required to have bylaws at formation and to maintain good standing to remain in compliance.

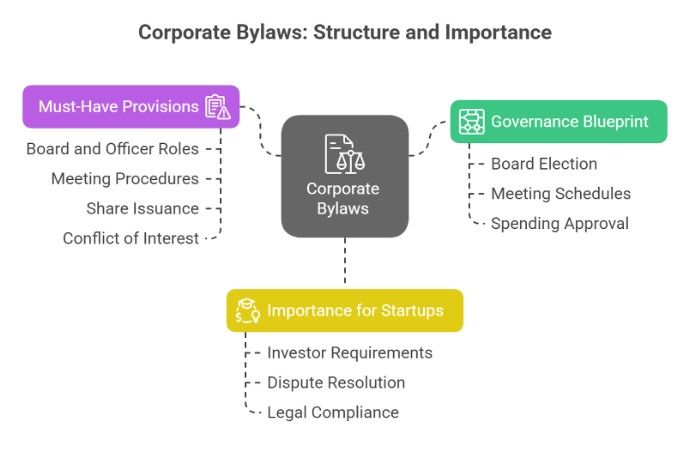

The Governance Blueprint for Your Corporation

Bylaws act as your company’s rulebook. They describe how your business will make important decisions, who has the authority to act, and how meetings and votes are handled.

You will use them to explain the roles of founders, directors, and officers. Bylaws answer questions such as:

- How will the board of directors be elected and replaced?

- When will shareholder and board meetings be held?

- Who gets to sign checks or approve spending?

In Texas, when forming a corporation, you are required to have bylaws to comply with state law and operate properly. You don’t have to file these rules with the government, but you do need to keep them in your records.

If you ever face conflicts or investor questions, well-written bylaws can keep things clear.

Must-Have Bylaw Provisions

Good bylaws for a startup company need to address several important areas. At a minimum, include:

- How board members and officers are chosen, removed, and what powers they hold

- How meetings happen, how votes are taken, and notification procedures

- When and how to issue or transfer shares

- How to handle conflicts of interest

- Rules for amending the bylaws

Some custom bylaws for startups even include rules on intellectual property and founder roles. Each business is unique, and you may want to tailor your bylaws to suit your industry or company size.

For example, a startup’s bylaws may include special provisions for remote meetings or digital voting.

Why Startups Still Need Bylaws (Even If You’re Small Now)

If your business is just you and a friend, bylaws might seem unnecessary at first. But even small startups need to have this document from the start for several key reasons.

First, investors and banks often require a copy of your bylaws before offering funding or opening a business account.

Second, bylaws help you settle disputes quickly, especially if co-founders disagree or someone leaves.

They make it clear how significant decisions, such as bringing on new partners, should be made. Having proper bylaws is also required in many states.

For instance, Texas law requires corporations to create and follow bylaws to remain compliant. If you wait until later, it may be more difficult to agree on the rules when issues arise.

Writing clear bylaws early on gives your startup a strong legal and practical foundation.

LLCs, Startups, and Solo Founders: Do You Still Need These Documents?

Even if you run your business alone or with a small team, having the right documents matters.

Agreements and internal rules help protect you, set clear expectations, and prepare you for banks, partners, and future growth.

Yes, And Here’s Why

If you form an LLC in Texas, you are not required by state law to create an operating agreement or bylaws. But skipping these documents can cause real problems.

A single-member LLC operating agreement in Texas is especially helpful. It defines how your business operates and demonstrates to others that your LLC is a genuine, separate legal entity.

Without an agreement, courts might not respect your liability protections. For startups with more than one founder, a founder agreement and company bylaws set rules for ownership, profits, and decision-making.

This avoids confusion and fights later. Even if you trust your partners, written agreements keep things clear when things get tough.

You are also more likely to attract the right help, since mentors and consultants often expect these documents.

The IRS, Banks, and Investors Expect Them

Before you can open a bank account for your LLC, most banks will ask for your operating agreement. This is true for both solo and multi-founder LLCs, regardless of whether they are located in Texas or elsewhere.

The IRS wants to know how your business is managed. An operating agreement proves that your LLC exists as a legitimate business, which is especially important for tax purposes and audits.

If you start a second LLC, the IRS also requires a separate EIN for each, and each should have its documents, not reused or recycled. If you want to raise money, investors will expect to see a clear founder agreement and bylaws.

They want to understand your structure, who makes decisions, and how conflicts are resolved.

According to legal guides for startups, being prepared with the right documents can make due diligence much easier if you ever seek outside investment or partnership.

Launching a business with partners? Let Surge Business Law draft your founder agreement to prevent future headaches. Schedule a call today.

Founder Disputes and Legal Risks: What Happens Without Proper Agreements?

Without clear founder agreements and bylaws, your business is significantly more likely to encounter serious legal and financial issues.

You can avoid costly mistakes that break apart startups or drain resources by taking simple legal steps early.

Common Disasters (And Lawsuits) That Could Have Been Avoided

When you don’t put roles, ownership, and responsibilities in writing, confusion can turn friends into rivals.

One founder might believe they own a greater share of the company than another, leading to arguments over ownership or decision-making authority.

Frequent legal risks include:

- Disputes about company direction

- Battles over intellectual property ownership

- Lawsuits after a co-founder leaves

- Fights over how company profits get split

A lack of legal structure often means disagreements become costly legal battles.

Valuable company assets like trademarks or product designs can end up claimed by the wrong person, risking everything you worked for.

In some cases, missing agreements can even prevent your business from raising money or growing beyond the first major hurdle.

How Surge Business Law Prevents These Issues

Surge business law fixes these risks before they happen.

If you use clear founder agreements and bylaws, it’s much easier to settle disputes and clarify your rights.

Here’s what these documents do:

- Define each founder’s role and ownership

- Set rules for decision-making

- Explain what happens if someone leaves

- Protect the business’s ideas and information

With everything in black and white, you reduce the chance of misunderstandings or lawsuits.

This makes your startup more attractive to investors and founders.

Legal documents also give you a clear process for handling problems, so you’re less likely to lose control of your company during disagreements.

Getting It Right: Drafting Founder Agreements and Bylaws That Hold Up

Founder agreements and bylaws give your startup clear rules and protect everyone’s rights.

Choosing the right method to create them, and the right legal help, can save you from mistakes and future headaches.

Why Templates and AI Docs Are Risky

Online templates and AI-generated legal forms may seem fast and inexpensive, but they come with hidden dangers.

Most templates are generic, so they rarely address your unique goals or state laws.

You may miss key details regarding founder responsibilities, equity splits, vesting schedules, or dispute resolution procedures.

Skipping these can create confusion or even spark costly lawsuits later.

AI-generated documents sometimes fail to keep pace with recent legal changes.

They won’t give you advice about things that matter, like which rules make sense for your business, or what to watch out for on your startup founder legal checklist.

If you want solid agreements and bylaws, you need advice built for your team and your state.

Otherwise, you risk paperwork that falls apart when problems come up.

What to Expect From Surge Business Law’s Flat-Fee Services

Austin founders can gain more peace of mind by working with a flat-fee startup lawyer instead of relying on templates.

With Surge Business Law’s flat-fee service, you know the exact price ahead of time and won’t face surprise costs.

The service usually covers:

- Custom founder agreements (equity, decision rules, IP protection)

- Bylaws designed for your specific business goals and growth plans

- Help with other legal documents for startup founders (NDAs, advisor agreements, etc.)

- Step-by-step reviews so you understand what every part means

You’ll get documents that meet legal requirements, reflect your real-world needs, and are easy to follow.

Having a lawyer explain and tailor these documents helps avoid mistakes and keeps your startup on solid ground as it grows.

Surge Business Law’s Local Legal Startup Packages

Obtaining the right legal assistance in Austin is crucial. Avoiding mistakes early can prevent problems for your business later.

Local firms, such as Surge Business Law, offer comprehensive legal startup packages that cover essential services like entity formation and drafting bylaws.

These packages also include drafting of founder or partnership agreements.

A typical package might include:

- Entity filing and registration with the State of Texas

- Custom bylaws or operating agreements

- Founder or partnership agreement drafting

- Initial legal consultations for compliance

Having an Austin business formation attorney walk you through these steps saves time.

They also keep you updated on local business requirements, so you stay compliant as Austin’s regulations change.

Be sure to ask for templates or examples tailored specifically to Texas law. Requirements may differ from other states.

Need legal docs that investors take seriously? Get bylaws and founder agreements done right with Surge Business Law—reach out for a free consultation.

Frequently Asked Questions

What is a founder agreement, and who needs one?

A founder agreement outlines the roles, equity, decision-making processes, and intellectual property (IP) ownership between co-founders. Any startup with more than one founder should establish a clear leadership structure.

Are bylaws required for all businesses in Texas?

Bylaws are required for corporations under Texas law and are highly recommended for LLCs to guide governance, protect against liability, and meet the requirements of banks or investors.

What’s the difference between bylaws and an operating agreement?

Bylaws govern corporations, while operating agreements govern LLCs. Both serve as internal rules that outline roles, responsibilities, and legal procedures.

What happens if co-founders don’t have an agreement?

Without a founder agreement, disputes over ownership, responsibility, or exit can lead to lawsuits, business shutdowns, or the loss of intellectual property (IP).

Can I use a free template for founder agreements?

Templates lack legal enforceability, state compliance, and customization. It’s particularly risky for startups, especially those seeking investors or seeking to grow.

How much does a founder agreement cost with a law firm?

At Surge Business Law, founder agreements are offered at flat fees, so no surprise bills. Prices typically start under $1,000, depending on complexity.